- 929.50 KB

- 2022-07-30 发布

- 1、本文档由用户上传,淘文库整理发布,可阅读全部内容。

- 2、本文档内容版权归属内容提供方,所产生的收益全部归内容提供方所有。如果您对本文有版权争议,请立即联系网站客服。

- 3、本文档由用户上传,本站不保证质量和数量令人满意,可能有诸多瑕疵,付费之前,请仔细阅读内容确认后进行付费下载。

- 网站客服QQ:403074932

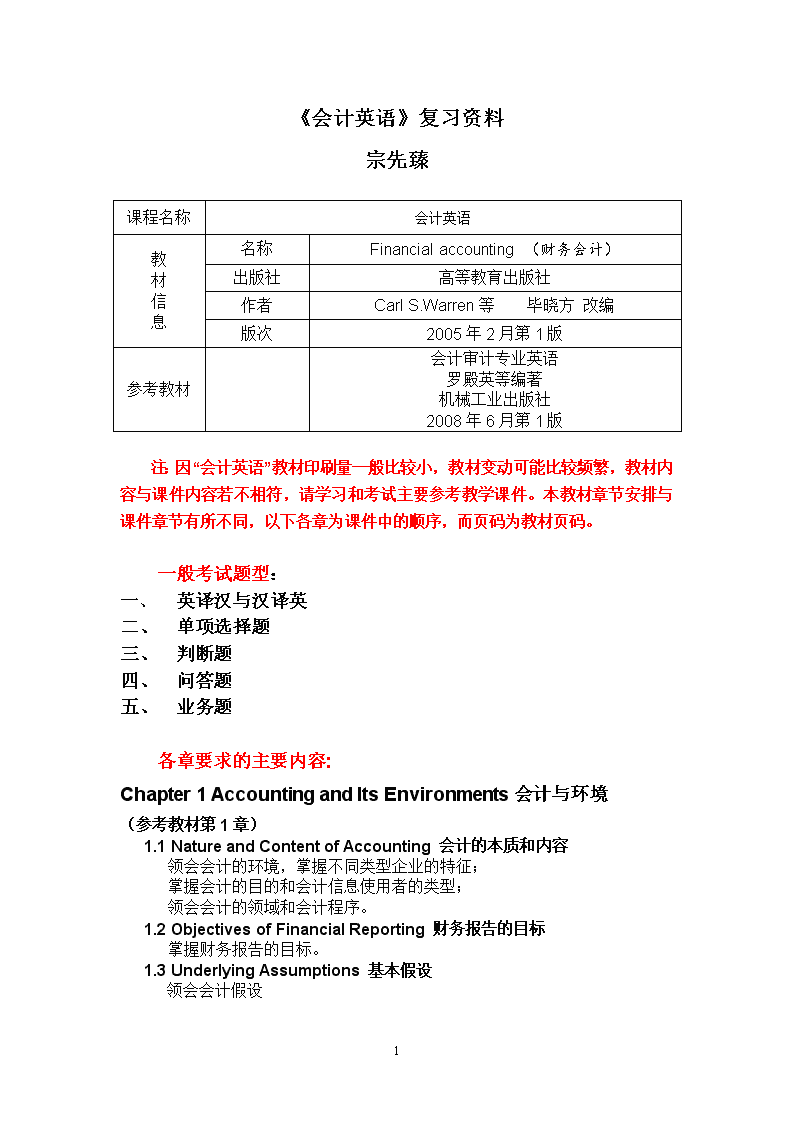

《会计英语》复习资料宗先臻课程名称会计英语教材信息名称Financialaccounting(财务会计)出版社高等教育出版社作者CarlS.Warren等毕晓方改编版次2005年2月第1版参考教材会计审计专业英语罗殿英等编著机械工业出版社2008年6月第1版注:因“会计英语”教材印刷量一般比较小,教材变动可能比较频繁,教材内容与课件内容若不相符,请学习和考试主要参考教学课件。本教材章节安排与课件章节有所不同,以下各章为课件中的顺序,而页码为教材页码。一般考试题型:一、英译汉与汉译英二、单项选择题三、判断题四、问答题五、业务题各章要求的主要内容:Chapter1AccountingandItsEnvironments会计与环境(参考教材第1章)1.1NatureandContentofAccounting会计的本质和内容领会会计的环境,掌握不同类型企业的特征;掌握会计的目的和会计信息使用者的类型;领会会计的领域和会计程序。1.2ObjectivesofFinancialReporting财务报告的目标掌握财务报告的目标。1.3UnderlyingAssumptions基本假设领会会计假设64\nChapter2AccountingConceptsandPrinciples会计概念与原则(参考教材第1章)2.1QualitativeCharacteristicsofUsefulAccountingInformation有用会计信息的质量特征了解会计信息的质量特征。2.2ElementsoftheFinancialStatements财务报表要素掌握财务报表要素的含义。2.3RecognitionandMeasurementPrinciples确认与计量的原则掌握财务报表要素的的确认与计量原则。Chapter3FinancialStatements财务报表(参考教材第1章和第16章)3.1BalanceSheet资产负债表领会资产负债表的定义和编制。3.2IncomeStatementandStatementofChangesinEquity利润表与所有者权益变动表领会收益表的定义和编制,了解所有者权益变动表的编制。3.3StatementofCashFlows现金流量表领会现金流量表的含义和编制方法。Chapter4AccountingCycle会计循环(参考教材第1章至第4章)4.1Theaccountingequation会计等式掌握会计等式的结构和经济业务对等式的影响。4.2Double-EntryBookkeeping复式簿记掌握复式记账法的应用。4.3TransactionsandBalanceSheetAccounts经济业务与资产负债表账户能够分析企业的经济业务,并能领会其影响。4.4JournalizingandPosting登记日记账与过账能够在日记账中编制分录,并过账。4.5TrialBalance试算表领会试算表的用途和编制4.6TheNeedforAdjustingEntries调整分录掌握调整分录的编制方法,领会其影响。4.7TheWorkSheet工作底稿了解工作底稿的用途和编制。64\n4.8TheClosingProcess结账掌握结账分录的用途和编制方法。Chapter5CurrentAssets流动资产(参考教材第7章、第8章和第9章)5.1Cash现金领会现金的内容和内部控制方法,理解领用现金的会计处理。5.2CurrentReceivables短期应收款项理解应收款的分类;掌握应收账款坏账的处理方法。5.3Inventory存货了解存货的种类;掌握存货的盘存制度;掌握存货成本流动假设和计价方法;了解存货估计方法。Chapter6Investments,PlantAssetsandIntangiblesAssets投资、固定资产与无形资产(参考教材第10章、第14章和第15章)6.1InvestmentsinEquityandDebtSecurities权益性与债务性证券投资领会证券的分类和投资类型;领会投资的目的和投资的计价;掌握证券投资的会计处理方法6.2PlantAssets(FixedAsset)固定资产领会固定资产的特点;掌握固定资产的折旧方法;领会固定资产处置的方法。6.3Intangibles无形资产领会无形资产的特征;了解无形资产的确认与摊销;领会资本性支出与收益性支出的划分意义。6.4NaturalResourcesandDepletion自然资源与折耗了解自然资源折耗的会计处理。Chapter7Liabilities负债(参考教材第11章和第15章)7.1CurrentLiabilities流动负债掌握金额确定的流动负债的会计处理;领会金额取决于经营成果的流动负债的会计处理。7.2BondsPayableandConvertibleBonds应付债券与可转换债券掌握公司债券的会计内容;理解可转换债券;64\n掌握长期债券投资的会计处理。Chapter8Owners’Equity所有者权益(参考教材第12章)8.1ContributedCapital实收资本领会公司的特征;领会各类股东的权利;掌握股票发行的会计处理;理解股票分割的意义。8.2RetainedEarnings留存收益掌握各类股利的特征和会计处理方法;领会库藏股的会计方法。Chapter9Performance经营成果(参考教材第6章和第14章)9.1Income收益领会收入与利得的区别;掌握收入的确认、计量和会计处理方法。9.2Expenses费用掌握费用的确认、计量和会计处理方法。9.3UnusualItems非正常项目了解不同非常项目的意义和会计处理。Chapter10FinancialStatementAnalysis财务报表分析(参考教材第17章)10.1FrameworkforFinancialStatementAnalysis财务报表分析框架领会财务报表分析的目的和各个报表的作用。10.2TechniquesofAnalysis分析技术掌握财务报表的分析方法——横向分析、纵向分析和比率分析。64\n一、英译汉与汉译英:第一章Business企业P2参见P2Soleproprietorship独资企业P3参见P3Partnership合伙P3参见P3Corporation公司P3参见P3Accounting会计P6参见P6Accountingprocess会计程序参见P7Financialaccounting财务会计P10参见P10Managerialaccounting管理会计P10参见P10Balancesheet资产负债表P17参见P17Incomestatement收益表(利润表)P17参见P17Statementofcashflow现金流量表参见P17Financialstatement财务报表P17参见P17Accrualbasis应计制(权责发生制)P71参见P71Cashbasis现金制(收付实现制)P71参见P71Economicentity/businessentity经济实体、会计主体P11参见P11Goingconcern持续经营Unitofmeasurement货币计量P12参见P12Accountingperiod会计期间P71参见P71第二章Asset资产P32参见P32Liability负债P32参见P32Equity权益P32参见P32Revenue收入P33参见P33Expense费用P33参见P33Income收益P18参见P18Historicalcost历史成本Currentcost现行成本Presentvalue现值381参见P381Realizablevalue可实现价值Incometax所得税参见P350Financialposition财务状况Performance业绩64\n第三章Currentassets流动资产99参见P99Currentliabilities流动负债99参见P99Accruedliability应计负债72参见P72Administrativeexpense管理费用161参见P161Depreciation折旧79参见P79Intangibleassets无形资产272参见P272Non-currentasset(fixedasset)非流动资产(固定资产)259参见P259Property,plantandequipment厂场资产259参见P259第四章Operatingcycle经营循环158参见P158Accountingcycle会计循环94参见P94Account账户32参见P32Accountingequation会计等式12参见P12Trialbalance试算平衡(试算表)53参见P53Journal日记账35参见P35Ledger分类账32参见P32Adjustingentry调整分录72参见P72Debit借方33参见P33Credit贷方34参见P34Double-entrysystem复式记账法38参见P38Post过账40参见P40Deferredexpense递延费用72参见P72Deferredrevenue递延收入72参见P72Unearnedrevenue未赚得收入(预收收入、递延收入)72参见P72Accruedrevenue应计收入72参见P72Closingentry结账分录102参见P102第五章Cash现金193参见P193Check支票197参见P197Bankstatement银行对账单198参见P198BankReconciliation银行余额调节表200参见P200Pettycashfund零用现金、备用金202参见P20264\nCashequivalents现金等价物AccountsReceivable应收账款210参见P210OtherReceivables其他应收款210参见P210NotesReceivable应收票据210参见P210UncollectibleAccountsExpense坏账费用212参见P212Baddebt坏账212参见P212AllowanceMethod备抵法213AllowanceforDoubtfulAccounts备抵坏账213参见P212DirectWrite-OffMethod直接冲销法217参见P217ContraAssetaccount资产抵销账户213参见P213Inventory存货235参见P235Costflowassumption成本流动假设238参见P238AverageCostMethod平均成本法243参见P243First-in,First-out(FIFO)Method先进先出法240参见P240Last-in,First-out(LIFO)Method后进先出法241参见P241Periodicsystem定期盘存制161参见P161perpetualsystem永续盘存制161、236参见P161,P236第六章Investment投资361参见P361marketablesecurities有价证券361参见P361financialinstruments金融工具Debtsecurities债务性证券388参见P388Equitysecurities权益性证券361参见P361Tradingsecurities交易性证券361参见P361Available-for-salesecurities可供出售证券361参见P361Held-to-maturitydebtsecurities持有至到期债务性证券388参见P388Fairvalue公允价值Equitymethod权益法363参见P363Costmethod成本法363参见P363AccumulatedDepreciation累计折旧79参见P79ResidualValue残值261参见P261Straight-lineMethod直线法262参见P262Declining-BalanceMethod余额递减法263参见P263accelerateddepreciationmethods加速折旧法263参见P26364\nImpairmentofFixedAsset固定资产减值354参见P354Amortization摊销273参见P273CapitalExpenditures资本性支出265参见P265RevenueExpenditures收益性支出265参见P265第七章Accountspayable应付账款285参见P285Notespayable应付票据285参见P285ProductWarranty产品质量担保288参见P288bondsinkingfund公司债偿债基金387参见P387BondsPayable应付公司债券383参见P383Long-TermLiabilities长期负债bonds债券378参见P378Discount折价380参见P380Premium溢价383参见P383ConvertibleBonds可转换债券380参见P380第八章Owners’Equity所有者权益302参见P302Stockholder’equity股东权益302参见P302CommonStock普通股303参见P303PreferredStock优先股303参见P303AdditionalPaid-inCapital增缴资本、股本溢价302参见P302RetainedEarnings留存收益313参见P313TreasuryStock库藏股307参见P307StockSplits股票分割308参见P308CashDividend现金股利309参见P309stockdividend股票股利310参见P310第九章Performance业绩Revenue收入174参见P174Gains利得Expenses费用Recognition确认Measurement计量Operatingexpenses营业费用161参见P16164\nSellingexpenses销售费用161参见P161Administrativeexpenses管理费用161参见P161Profit利润Netincome净收益Sales销售收入158参见P158Salesdiscounts销售折扣159、165参见P159,P165Costofmerchandisesold销售成本159参见P159Grossprofit毛利161参见P161Losses损失Tradediscounts商业折扣172参见P172cashdiscounts现金折扣168参见P168Incometax所得税350参见P350UnusualItems非正常项目353参见P353第十章Common-SizeStatements共同比报表440参见P440HorizontalAnalysis横向分析436参见P436trendanalysis趋势分析436参见P436VerticalAnalysis纵向分析438参见P438Profitability获利能力441参见P441Solvency偿债能力441参见P441AccountsReceivableTurnover应收账款周转率444参见P444CurrentRatio流动比率442参见P442InventoryTurnover存货周转率444参见P444QuickAssets速动资产443参见P443RateEarnedonStockholders’Equity股东权益报酬率449参见P449EarningsperShareonCommonStock普通股每股收益450参见P450RateEarnedonTotalAssets总资产报酬率448参见P448Leverage财务杠杆Price-Earnings(P/E)Ratio市盈率450参见P450WorkingCapital营运资本442参见P44264\n二、单项选择(红字为正确答案):Financialreportsareusedbya.managementb.creditorsc.investorsd.alloftheabove★考核知识点:企业利益相关者P6参见P6附2.8参考课件第1章Stakeholdersuseaccountingreportsasaprimarysourceofinformationonwhichtheybasetheirdecisions.Thestakeholdersincludeowners,managers,employees,customers,creditors,governmentagencies.1.Foraccountingpurposes,thebusinessentityshouldbeconsideredseparatefromitsownersiftheentityis()a.acorporationb.aproprietorshipc.apartnershipd.alloftheabove★考核知识点:会计假设(会计主体)P11参见P112.Whichofthefollowingbestdescribesaccounting?a.recordseconomicdatabutdoesnotcommunicatethedatatousersaccordingtoanyspecificrulesb.isaninformationsystemthatprovidesreportstostakeholdersc.isofnousebyindividualsoutsideofthebusinessd.isusedonlyforfillingouttaxreturnsandforfinancialstatementsforvarioustypeofgovernmentalreportingrequirements★考核知识点:会计P6参见P63.Usingaccrualaccounting,expensesarerecordedandreportedonlya.whentheyareincurred,whetherornotcashispaidb.whentheyareincurredandpaidatthesametimec.iftheyarepaidbeforetheyareincurredd.iftheyarepaidaftertheyareincurred★考核知识点:应计制P71参见P714.Themeasurementbasesexclude()a.Historicalcost64\nb.Currentcostc.Salepriced.Presentvalue★考核知识点:会计计量5.Debtsowedbyabusinessarereferredtoas()a.accountsreceivablesb.equitiesc.owner’sequityd.liabilities★考核知识点:负债P12参见P126.Whichofthefollowingfinancialstatementsreportsinformationasofaspecificdate?a.incomestatemenb.statementofowner'sequityc.balancesheetd.statementofcashflows★考核知识点:资产负债表P17参见P177.Cashinvestmentsmadebytheownertothebusinessarereportedonthestatementofcashflowsinthea.financingactivitiessectionb.investingactivitiessectionc.operatingactivitiessectiond.supplementalstatement★考核知识点:现金流量表P20参见P208.Theaccountingequationmaybeexpressedasa.Assets=Equities-Liabilitiesb.Assets+Liabilities=Owner'sEquityc.Assets=Revenues-Liabilitiesd.Assets-Liabilities=Owner'sEquity★考核知识点:会计等式P12参见P129.Whichofthefollowinggroupsofaccountshaveanormalcreditbalance?a.revenues,liabilities,capitalb.capital,assetsc.liabilities,expenses64\nd.assets,expenses★考核知识点:帐户结构P34参见P3410.Whichofthefollowinggroupsofaccountshaveanormaldebitbalance?a.revenues,liabilities,capitalb.capital,assetsc.liabilities,expensesd.assets,expenses★考核知识点:帐户结构P34参见P3411.Whichofthefollowingtypesofaccountshaveanormalcreditbalance?a.assetsandliabilitiesb.liabilitiesandexpensesc.revenuesandliabilitiesd.capitalanddrawing★考核知识点:帐户结构P34参见P3412.Intheaccountingcycle,thelaststepis()a.preparingapost-closingtrialbalanceb.preparingthefinancialstatements#c.journalizingandpostingtheadjustingentriesd.journalizingandpostingtheclosingentries考核知识点:会计循环P95参见P95(7)Apost-closingtrialbalanceisprepared.13.Whichofthefollowingshouldnotbeconsideredcashbyanaccountant?a.coinsb.bankcheckingaccountsc.postagestampsd.Pettycashfunds考核知识点:现金P193参见P19314.Abankreconciliationshouldbepreparedperiodicallybecause()a.thedepositor'srecordsandthebank'srecordsareinagreementb.thebankhasnotrecordedallofitstransactionsc.anydifferencesbetweenthedepositor'srecordsandthebank'srecordsshouldbedetermined,andanyerrorsmadebyeitherpartyshouldbediscoveredandcorrectedd.thebankmustmakesurethatitsrecordsarecorrect考核知识点:银行余额调节表P200参见P20015.Theamountoftheoutstandingchecksisincludedonthebank64\nreconciliationasa(n)()a.deductionfromthebalanceperdepositor'srecordsb.additiontothebalanceperbankstatementc.deductionfromthebalanceperbankstatementd.additiontothebalanceperdepositor'srecords考核知识点:银行余额调节表P200参见P20016.Theassetcreatedbyabusinesswhenitmakesasaleonaccountistermeda.accountspayableb.prepaidexpensec.accountsreceivabled.unearnedrevenue★考核知识点:应收账款P15、210参见P15,P21017.WhatisthetypeofaccountandnormalbalanceofAllowanceforDoubtfulAccounts?a.Contraasset,creditb.Asset,debitc.Asset,creditd.Contraasset,debit★考核知识点:应收账款坏账P213参见P21318.Theterm"inventory"indicates()a.merchandiseheldforsaleinthenormalcourseofbusinessb.materialsintheprocessofproductionorheldforproductionc.suppliesd.bothAandB★考核知识点:存货P235参见P23519.Merchandiseinventoryattheendoftheyearwasunderstated.Whichofthefollowingstatementscorrectlystatestheeffectoftheerror?a.netincomeisunderstatedb.netincomeisoverstatedc.costofmerchandisesoldisunderstatedd.merchandiseinventoryreportedonthebalancesheetisoverstated★考核知识点:存货P237参见P23720.Merchandiseinventoryattheendoftheyearisoverstated.Whichofthefollowingstatementscorrectlystatestheeffectoftheerror?a.costofmerchandisesoldisoverstatedb.owner'sequityisoverstatedc.grossprofitisunderstated64\nd.netincomeisunderstated★考核知识点:存货P237参见P23721.Theinventorymethodthatassignsthemostrecentcoststocostofgoodsoldisa.FIFOb.LIFOc.averaged.specificidentification★考核知识点:存货P241参见P24122.Underwhichmethodofcostflowsistheinventoryassumedtobecomposedofthemostrecentcosts?a.averagecostb.first-in,first-outc.last-in,first-outd.weightedaverage★考核知识点:存货P240参见P24023.Whentheperpetualinventorysystemisused,theinventorysoldisdebitedto()a.suppliesexpenseb.costofmerchandisesoldc.merchandiseinventoryd.sales★考核知识点:存货P238-241参见P238-P24124.Allofthefollowingbelowareneededforthecalculationofdepreciationexcepta.costb.residualvaluec.estimatedlifed.bookvalue★考核知识点:折旧P261参见P26125.Acharacteristicofafixedassetisthatitisa.intangibleb.usedintheoperationsofabusinessc.heldforsaleintheordinarycourseofthebusinessd.noneoftheabove★考核知识点:固定资产特征P259参见P25926.AccumulatedDepreciation()a.isusedtoshowtheamountofcostexpirationofintangiblesb.isthesameasDepreciationExpensec.isacontraassetaccountd.isusedtoshowtheamountofcostexpirationofnaturalresources★考核知识点:累计折旧P260参见P26064\n27.Thetwomethodsofaccountingforinvestmentsinstockarethecostmethodandthe()a.straight-linemethodb.equitymethodc.liabilitymethodd.interestmethod★考核知识点:股票投资P363参见P36328.Acapitalexpenditureresultsinadebitto()a.anexpenseaccountb.acapitalaccountc.aliabilityaccountd.anassetaccount★考核知识点:资本性支出P265参见P26529.Currentliabilitiesare()a.due,butnotreceivableformorethanoneyearb.due,butnotpayableformorethanoneyearc.dueandreceivablewithinoneyeard.dueandpayablewithinoneyear★考核知识点:流动负债P285参见P28530.Thedebtcreatedbyabusinesswhenitmakesapurchaseonaccountisreferredtoasana.accountreceivableb.accountpayablec.assetd.expensepayable★考核知识点:应付账款P285参见P28531.Notesmaybeissued()a.whenassetsarepurchasedb.tocreditor'stotemporarilysatisfyanaccountpayablecreatedearlierc.whenborrowingmoneyd.alloftheabove★考核知识点:应付票据P285-287参见P285-P28732.Thecostofaproductwarrantyshouldbeincludedasanexpenseinthea.periodthecashiscollectedforaproductsoldonaccountb.futureperiodwhenthecostofrepairingtheproductispaidc.periodofthesaleoftheproductd.futureperiodwhentheproductisrepairedorreplaced★考核知识点:产品质量担保P287-289参见P287-P28964\n33.Ifthemarketrateofinterestis8%,thepriceof6%bondspayinginterestsemiannuallywithafacevalueof$100,000willbea.Equalto$100,000b.Greaterthan$100,000c.Lessthan$100,000d.Greaterthanorlessthan$100,000,dependingonthematuritydateofthebonds★考核知识点:应付债券P380参见P38034.Theinterestratespecifiedinthebondindentureiscalledthe()a.discountrateb.contractratec.marketrated.effectiverate★考核知识点:应付债券P380参见P38035.Whenthecorporationissuingthebondshastherighttorepurchasethebondspriortothematuritydateforaspecificprice,thebondsarea.convertiblebondsb.unsecuredbondsc.debenturebondsd.callablebonds★考核知识点:可赎回债券P285参见P28536.Whenthemarketrateofinterestonbondsishigherthanthecontractrate,thebondswillsellata.apremiumb.theirfacevaluec.theirmaturityvalued.adiscount★考核知识点:应付债券P380参见P38037.Onepotentialadvantageoffinancingcorporationsthroughtheuseofbondsratherthancommonstockisa.theinterestonbondsmustbepaidwhendueb.thecorporationmustpaythebondsatmaturityc.theinterestexpenseisdeductiblefortaxpurposesbythecorporationd.ahigherearningspershareisguaranteedforexistingcommonshareholders★考核知识点:应付债券P378参见P37838.Characteristicsofacorporationinclude()a.shareholderswhoaremutualagentsb.directmanagementbytheshareholders(owners)c.itsinabilitytoownpropertyd.shareholderswhohavelimitedliability64\n★考核知识点:公司特征P300参见P30039.Stockholders'equity()a.isusuallyequaltocashonhandb.includespaid-incapitalandliabilitiesc.includesretainedearningsandpaid-incapitald.isshownontheincomestatement★考核知识点:股东权益P302参见P30240.Theexcessofissuepriceoverparofcommonstockistermeda(n)()a.discountb.incomec.deficitd.premium★考核知识点:股票溢价发行P306参见P30641.Cashdividendsareusuallynotpaidonwhichofthefollowing?a.classBcommonstockb.preferredstockc.treasurystockd.classAcommonstock★考核知识点:库藏股P307参见P30742.Whichofthefollowingaccountsbelowisreportedinthepaid-incapital/stockholders'equitysectionofthecorporatebalancesheet?a.Cashb.StockDividendsc.OrganizationalExpensesd.PreferredStock★考核知识点:股东权益P303参见P303附2.42参考课件第8章64\n43.Ifpreferredstockhasdividendsinarrears,thepreferredstockmustbea.participatingb.callablec.cumulatived.convertible★考核知识点:累积优先股P304参见P30444.Theprimarypurposeofastocksplitistoa.increasepaid-incapitalb.reducethemarketpriceofthestockpersharec.increasethemarketpriceofthestockpershared.increaseretainedearnings★考核知识点:股票分割P308参见P30845.Whichstatementbelowisnotareasonforacorporationtobuybackitsownstock.a.resaletoemployeesb.bonustoemployeesc.forsupportingthemarketpriceofthestockd.toincreasethesharesoutstanding★考核知识点:库藏股P307参见P30746.Theliabilityforadividendisrecordedonwhichofthefollowingdates?64\na.thedateofrecordb.thedateofpaymentc.thedateofannouncementd.thedateofdeclaration★考核知识点:股利P309参见P30947.Incredittermsof2/10,n/30,the"2"representsthea.numberofdaysinthediscountperiodb.fullamountoftheinvoicec.numberofdayswhentheentireamountisdued.percentofthecashdiscount★考核知识点:现金折扣P165-168参见P165-P16848.Revenueshouldberecognizedwhen()a.cashisreceivedb.theserviceisperformedc.thecustomerplacesanorderd.thecustomerchargesanorder★考核知识点:收入49.Theabilityofabusinesstopayitsdebtsastheycomedueandtoearnareasonableamountofincomeisreferredtoas()a.solvencyandleverageb.solvencyandprofitabilityc.solvencyandliquidityd.solvencyandequity★考核知识点:报表分析P441参见P44150.Whichofthefollowingisnotincludedinthecomputationofthequickratio?a.Inventoryb.marketablesecuritiesc.accountsreceivabled.Cash★考核知识点:速动比率P443参见P443四、问答题:1.Thecharacteristicsofsoleproprietorship,partnershipandcorporations简要说明独资、合伙和公司的优缺点。★考核知识点:企业组织形式P3参见P3附4.1参考课件第1章64\n2.Whatistheroleofaccounting.简述会计的作用。★考核知识点:会计的作用P6参见P6附4.2参考课件第1章3.Differentiatebetweenfinancialaccountingandmanagerialaccounting.财务会计与管理会计的区别。参考答案:Financialaccountingisprimarilyconcernedwiththerecordingandreportingofeconomicdataandactivitiesforabusiness.Managementaccountingusesbothfinancialaccountingandestimateddatatoaidmanagementinrunningday-to-dayoperationsandinplanningfutureoperations..★考核知识点:财务会计与管理会计P10参见P10附4.3参考课件第1章4.Theobjectiveoffinancialreporting财务报告的目标。参考答案:Overallobjective(总体目标)offinancialreportingistoprovidefinancialinformationusefultoexternalusersinmakingeconomicdecisions.(a)provideinformationaboutthefinancialposition,performanceandchangesinfinancialpositionofanentitythatisusefultoawiderangeofusersinmakingeconomicdecisions;(向使用者提供有关企业财务状况、经营成果和财务状况变动情况的信息,以利于其作出经济决策。)(b)showtheresultsofthestewardshipofmanagement,ortheaccountabilityofmanagementfortheresourcesentrustedtoit.(反映管理当局受托责任的履行结果,或管理当局受托管理资源的责任。)★考核知识点:财务报告的目标参见P22附4.4参考课件第1章5.Whataretherecognitionandmeasurementprinciples?财务报表要素的确认与计量原则。参考答案:(1)Recognitionistheprocessofincorporatinginthebalancesheetorincomestatementanitemthatmeetthedefinitionofanelementandsatisfiestherecognitioncriteria.RecognitionCriteria确认标准:a.TheProbabilityofFutureEconomicBenefit未来经济利益流入的可能性b.MeasurementReliably计量的可靠性64\n(2)Measurementistheprocessofdeterminingthemonetaryamountsatwhichtheelementsoffinancialstatementsaretoberecognizedandcarriedinthebalancesheetorincomestatement.MeasurementBases计量基础:a.Historicalcost.历史成本b.Currentcost现行成本c.Realizable(settlement)value可实现(清算)价值d.Presentvalue现值★考核知识点:确认与计量原则参见P11附4.5参考课件第1章6.Thetypesofcashflowactivitiesreportedinthestatementofcashflows.现金流量表包括哪几部分?★考核知识点:现金流量表P405参见P405附4.6参考课件第3章7.Differentiatebetweentheindirectmethodandthedirectmethod.简述经营活动现金流量的直接法与间接法的优缺点。★考核知识点:现金流量表P406参见P406附4.7参考课件第3章8.Differentiatebetweentheaccrualbasisandthecashbasis.应计制与现金制的区别。参考答案:Undertheaccrualbasisfortheaccountingperiodconcept,revenuesarereportedintheincomestatementintheperiodinwhichtheyareearned.Underthecashbasisfortheaccountingperiodconcept,revenuesandexpensesarereportedintheincomestatementintheperiodinwhichcashisreceivedorpaid.★考核知识点:应计制与现金制P71参见P71附4.8参考课件第1章、第4章9.Whatisthedouble-entrysystem?简述复式记账法的含义参考答案:lAsystemofrecordingtransactionsinawaythatmaintainstheequalityoftheaccountingequation.64\nlThefundamentalruleofdouble-entrybookkeepingisthatdebitsmustequalcredits.lForeverytransaction,theremustbeatleastonedebitandonecredit.lDebitsmustalwaysequalcreditsforeachtransaction.lDebitsarealwaysenteredontheleftsideofanaccountandcreditsarealwaysenteredontherightside.★考核知识点:复式记账法P38参见P38附4.9参考课件第4章10.Whatarethemajortypesofadjustingentries?调整分录的种类参考答案:Adjustingentriescanbeclassifiedaseither:PrepaymentsorAccruals(1)Prepaymentsfallintotwocategories:a.Prepaidexpenseb.DeferredRevenue(UnearnedRevenue)(2)Accrualsfallintotwocategoriesa.Accruedexpensesb.Accruedrevenues★考核知识点:调整分录P72参见P72附4.10参考课件第4章Companiesareonacalendarorfiscalyearandbusinesstransactionscancutacrosstwoyears.Therefore,adjustingentriesareneededtoensurethattherevenuerecognitionandmatchingprinciplesarefollowed.Adjustingentriescanbeclassifiedaseither:PrepaymentsorAccruals(1)Prepaymentsfallintotwocategories:a.Prepaidexpenses:expenseshavebeenpaidincashandarerecordedasassetsuntiltheyareusedorconsumed.b.DeferredRevenue(UnearnedRevenue):Revenuesreceivedincashandrecordedasliabilitiesbeforetheyareearned.(2)Accrualsfallintotwocategoriesa.Accruedexpensesareexpensesthathavebeenincurredbutnotyetpaidincashandthereisnooriginalentry.b.Accruedrevenuesarerevenuesthathavebeenearnedbutnotyetreceivedincash.11.Describethebasicstepsoftheaccountingcycle.简述会计循环的步骤。参考答案:Theaccountingcycle(oraccountingprocess)includesstandardizedproceduresthatareperformedinsequenceduringeveryperiod.(会计循环,或称为会计程序,是在每个会计期间按照一定顺序处理业务的一套规范化的程序)64\nItiscalledcyclebecausethestepsrepeatedeachaccountingperiod.(1)Transactionsareanalyzedandrecordedinthejournal.(2).Transactionsarepostedtotheledger.(3)Atrialbalanceisprepared,adjustmentdataareassembled,andanoptionalworksheetiscompleted.(4)Financialstatementsareprepared.(5)Adjustingentriesarejournalizedandposted.(6)Closingentriesarejournalizedandposted.(7)Apost-closingtrialbalanceisprepared.★考核知识点:会计循环P95参见P95附4.10参考课件第4章11.Whatarethemethodsofcontrolofcash?现金的内部控制方法。★考核知识点:调整分录P72参见P72附4.11参考课件第4章12.Whataretheadvantagesoftheallowancemethodforuncollectibleaccounts?应收账款坏账备抵法的优点。★考核知识点:应收账款坏账处理P212-217参见P212-P217附4.12参考课件第5章Managementmakesanestimateeachyearoftheportionofaccountsreceivablethatmaynotbecollectible.UncollectibleAccountsExpense(BadDebts)isdebitedandAllowanceforDoubtfulAccountsiscredited.ActualaccountsthatprovetobeuncollectiblearedebitedtoAllowanceforDoubtfulAccountsandcreditedtoAccountsReceivable.(1)Thismethodisconsistentwiththematchingprinciple.(2)Theaccountsreceivablestateatnetrealizablevalueatendoftheaccountingperiod.13.Describethecharacteristicsoftheperiodicinventorysystemandtheperpetualinventorysystem.存货的两种盘存制度的特点。参考答案:Acompanyusingaperpetualsystemmaintainsacontinuousrecordofthephysicalquantitiesinitsinventory.Acompanyusingaperiodicsystemdoesnotmaintainsacontinuousrecordofthephysicalquantitiesonhand.1.Inaperiodicinventorysystem,whenanitemissold,theonlyjournalentryrecordedistoreflectthesaleofthemerchandiseCostofgoodssoldisrecordedonlyaftertheendinginventoryhasbeencountedand64\nvaluedattheendoftheperiod.1.Withaperpetualinventorysystem,continuallyupdatedrecordsaremaintainedforinventoryitems.Suchtrackingisreadilyenabledthroughadvancesintechnology.Asaresult,twojournalentriesaremadewhenasaleoccurs.★考核知识点:存货盘存制度P236参见P236附4.13参考课件第5章14.Whatarethefinancialstatementseffectsofinventorymethods?存货计价方法对报表有何影响?(以先进先出法、后进先出法和平均成本法为例)(1)IncomeStatementEffects:Inperiodsofincreasingprices,FIFOreportsthehighestnetincome,LIFOthelowestnetincome,andaveragecostfallsinthemiddle.Inperiodsofdecreasingprices,theconverseistrue:FIFOwillreportthelowestnetincome,LIFOthehighest,withaveragecostinthemiddle.(2)BalanceSheetEffects:Inaperiodofinflation,thecostsallocatedtoendinginventoryusingFIFOwillapproximatecurrentcosts.Thus,themarkettobookvalueoftheinventoryshouldapproximate1.0.Conversely,duringaperiodofincreasingprices,thecostsallocatedtotheendinginventoryusingLIFOwillbesignificantlyunderstated.Thus,themarkettobookratiowillbegreaterthan1.0.★考核知识点:存货计价方法P237-244参见P237-P244附4.14参考课件第5章15.Whataretheclassificationsandobjectivesofinvestmentinsecurities?简述证券投资的类型和目的。参考答案:ClassificationsofInvestments:Tradingsecurities;Held-to-maturitydebtsecurities;Available-for-salesecuritiesObjectivesofInvestmentinSecurities:(1)Temporaryinvestmentofsurpluscash(2)Investmentsolelyforareturn(3)Investmentforinfluence(4)Purchaseforcontrol★考核知识点:存货计价方法P237-244参见P237-P244附4.15参考课件第6章Marketablesecurities–Stocks,bondsandotherfinancialinstrumentsthatorganizationsholdinlieuofcash.Thesearealsoreferredtointhefinancialstatementsasshort-terminvestmentsTwoTypesofMarketablesecurities:64\nDebtsecurities-Thesearebondsissuedbycorporationsorgovernmentthathavematurityvalue,interestrateandmaturitydate.Equitysecurities–Theseareanysecurities,suchascommonsharesthatrepresentownershipinacompany.ClassificationsofInvestmentsinEquityandDebtSecurities:(1)Tradingsecurities:Investmentsatfairvaluethroughprofitorloss;heldfortrading,ordesignatedtobe‘atfairvaluethroughprofitorloss’(2)Held-to-maturitydebtsecurities:financialassetswithfixedordeterminablepayments;fixedmaturity;positiveintentandabilitytoholdtomaturity(3)Available-for-salesecurities:remainingfinancialassets;donotfallintoanyofthetwocategoriesaboveObjectivesofInvestmentinSecurities(1)Temporaryinvestmentofsurpluscash(2)Investmentsolelyforareturn(3)Investmentforinfluence(4)Purchaseforcontrol16.Describethereasonsforholdingmarketablesecurities.简述企业进行短期有价证券投资的原因★考核知识点:短期投资P361参见P361附4.16参考课件第6章Therearemanyreasonswhyacompanymaywanttobuydebtorequitysecuritiesfromanothercompany.Forexample,CompanyAmaypurchasethedebtofCompanyBbecause•CompanyB’sdebtispayingagoodinterestrate.•ThedebtmayhaveamaturitydatethatmatchesCompanyA’sneedforcash.•Thedebtmaybesellingforlessthanfacevalue,andCompanyAthinksthatitcansellthedebtlateratagain.Investmentsindebtandequitysecuritiescanbeclassifiedonthestatementoffinancialpositionaseithercurrentornon-currentassets.Onereasonforholdingshortterminvestmentsrelatestothecontrolofcash.Theamountofcashheldbyanentityshouldbecarefullyregulatedsothatthereisneithertoomuchnortoolittleavailableatanytime.Ifthereistoolittlecashonhand,thefirmwillnotbeabletomeetdailyorperiodiccashrequirements;ifthereistoomuchcashonhand,aportionoftheentity’sassetsareunproductive.Therefore,managementwilltrytokeepjustenoughcashonhandatanyonetimetomeetdailyrequirements,plusacushionforemergencies.Cashinexcessofthedailyminimumshouldbeinvestedinincome-producingopportunities,suchasthedebtandequitysecuritiesofothercompanies.64\n17.Describethecharacteristicsofproperty,plantandequipment.简述固定资产的特点。★考核知识点:固定资产P259参见P259附4.17参考课件第6章Property,plant,andequipmentisdefinedastangibleassetsthatareheldforuseinproductionorsupplyofgoodsandservices,forrentalstoothers,orforadministrativepurposes;theyareexpectedtobeusedduringmorethanoneperiod.Includes:Land,Buildingstructures(offices,factories,warehouses),andEquipment(machinery,furniture,tools).Thecharacteristics:(1)“Usedinoperations”andnotforresale.(2)Long-terminnatureandusuallydepreciated.(3)Possessphysicalsubstance.18.Describethebenefitsofaccelerateddepreciationmethods.什么是加速折旧法?其优点有哪些?参考答案:Acceleratedmethodsofdepreciationresultinmoredepreciationintheearlyyearsofanasset'slifeandlessdepreciationinthelateryearsofanasset'slifethandoesthestraight-lineapproach.Thebenefitsofaccelerateddepreciationmethodsare:(1)Decreasingdepreciationchargesarematchedagainstincreasingrepairandmaintenancecharges.(2)Higherdepreciationchargesdrivenetincomedowninearlyyearsofanasset’slife.Asaresult,accelerateddepreciationmethodsarefavoredfortaxpurposes.★考核知识点:固定资产P263参见P263附4.18参考课件第6章19.Describethecharacteristicsofintangibleassets.什么是无形资产?其特征有哪些?参考答案:Anintangibleassetsisanidentifiablenon-monetaryassetwithoutphysicalsubstance.无形资产是指没有实物形态的、可辨认的非货币性资产。Examplesofintangibleassetsincludegoodwill,patents,copyrights,franchises,trademarksandtradenames……例如:商誉、专利权、版权、特许权、商标、商号等Thecharacteristics:(1)ahigherdegreeofuncertaintyregardingthefuturebenefits未来收益的高度不确定性(2)valuesubjecttowiderfluctuations价值波动性大(3)havingvalueonlytoaparticularcompany其价值只与某一特定企业相关64\n(1)‘non-monetary’feature非货币性质★考核知识点:无形资产P272参见P272附4.19参考课件第6章如下答案也可以:Intangibleassetsarerights,privileges,andcompetitiveadvantagesthatresultfromownershipoflong-livedassetsthatdonotpossessphysicalsubstance.Examplesofintangibleassetsincludegoodwill,patents,copyrights,franchises,trademarksandtradenames……TheMainCharacteristics:(1)Identifiable.可辨认性(2)Lackphysicalexistence.缺乏实物形态(3)Notmonetaryassets.非货币性资产Normallyclassifiedasnon-currentasset.20.Describethereasonsforissuanceoflong-termliabilities.举借长期债务的原因(与发行股票相比)。参考答案:ReasonsforIssuanceofLong-TermLiabilities:(1)Debtfinancingmaybetheonlyavailablesourceoffunds.(2)Debtfinancingmayhavealowercost.(3)Debtfinancingoffersanincometaxadvantage.(4)Thevotingprivilegeisnotshared.(5)Debtfinancingofferstheopportunityforleverage.★考核知识点:长期负债P378参见P378附4.20参考课件第7章Along-termliability:aliabilitywithrepaymenttermsextendingbeyondoneyearfromthecurrentbalancesheetdateortheoperatingcycleoftheborrower,whicheverislonger.Long-termdebtisoftenanattractivemeansoffinancingforthedebtor:(1)creditorsdonotacquirevotingprivilegesinthedebtorcompany,andissuanceofdebtcausesnoownershipdilution(2)debtcapitalisobtainedmoreeasilythanequitycapitalformanycompanies,especiallyprivatecompanies(3)interestexpense,unlikedividends,istaxdeductible(4)afirmthatearnsareturnonborrowedfundsthatexceedstherateitmustpayininterestisusingdebttoitsadvantageandissaidtobesuccessfullylevered(orleveraged)Leverageisdangerousifsalesorearningsdeclineandinterestexpensebecomesanincreasingpercentageofearnings.21.Thecharacteristicsofcorporations简述公司的特征64\n★考核知识点:公司特征P300参见P300附4.21参考课件第8章22.Describetherightsofcommonshareholders.(简述普通股股东的权利)★考核知识点:普通股P303参见P303附4.22参考课件第8章Thetwoprimaryclassesofpaid-incapitalarecommonstock(ordinaryshares)andpreferredstock.Theprimaryattractivenessofpreferredstocksisthattheyarepreferredovercommonastodividends.RightsandPrivilegeofShareholders:CommonShareholders(1)righttovoteonkeycorporatematters(2)preemptiverighttopurchaseenoughsharestoretaintheirproportionalownershipinterest(3)righttoshareproportionatelyinanydividends(4)haveresidualinterestinassetsinliquidationPreferredShareholders(1)stipulateddividendrate;stipulatedliquidationvalue(2)participationinearnings;cumulativefeature23.Describethethreeconditionsthatcorporationsdeclareandpaycashdividendsonsharesoutstanding.现金股利的发放条件。参考答案:Corporationsgenerallydeclareandpaycashdividendsonsharesoutstandingwhenthreeconditionsexist:1.Sufficientretainedearnings2.Sufficientcash3.Formalactionbytheboardofdirectors★考核知识点:现金股利P309参见P309附4.23参考课件第8章Dividendsaredistributionsofretainedearningstostockholders.Dividendsmaybepaidincash,stock,orproperty.Dividends,evenoncumulativepreferredstock,areneverrequired,butoncedeclaredbecomealegalliabilityofthecorporation.Corporationsgenerallydeclareandpaycashdividendsonsharesoutstandingwhenthreeconditionsexist:1.Sufficientretainedearnings2.Sufficientcash3.Formalactionbytheboardofdirectors64\n24.Describethereasonsexistforacompanytoissueastockdividend.公司发放股票股利的原因。参考答案:Numerousreasonsexistforacompanytoissueastockdividend:(1)toshowthatthefirmplanstopermanentlyretainaportionofearningsinthebusiness(2)toincreasethenumberofsharesoutstanding,whichreducesthemarketpricepershareandwhich,inturn,tendstoincreasetradingofsharesinthemarket.(alargestockdividends)(3)tocontinuedividenddistributionswithoutdisbursingassets(usuallycash)thatmaybeneededforoperations(4)stockdividendsdonotsubjecttheshareholderstoincometax(5)shareholdersmayactuallyprefertoreceivestockdividendsbecausetheycanselltheseadditionalsharesonlyiftheychoosetodoso★考核知识点:股票股利P310参见P310附4.24参考课件第8章Astockdividend:aproportionaldistributiontoshareholdersofadditionalcommonorpreferredsharesofthecorporationAstockdividenddoesnotchangetheassets,liabilities,ortotalshareholders'equityoftheissuingcorporationItdoesnotchangetheproportionateownershipofanyshareholderItsimplyincreasesthenumberofsharesoutstandingTheeffectofastockdividendonthestockholders’equityoftheissuingcorporationistotransferretainedearnings(themarketpriceoftheshares)topaid-incapital.Numerousreasonsexistforacompanytoissueastockdividend:(1)toshowthatthefirmplanstopermanentlyretainaportionofearningsinthebusiness(2)toincreasethenumberofsharesoutstanding,whichreducesthemarketpricepershareandwhich,inturn,tendstoincreasetradingofsharesinthemarket.(alargestockdividends)(3)tocontinuedividenddistributionswithoutdisbursingassets(usuallycash)thatmaybeneededforoperations(4)stockdividendsdonotsubjecttheshareholderstoincometaxshareholdersmayactuallyprefertoreceivestockdividendsbecausetheycanselltheseadditionalsharesonlyiftheychoosetodoso25.Differentiatebetweenthestockdividendsandstocksplits.股票股利与股票分割的区别。参考答案:StockDividends:(1)Parvalueofasharedoesnotchange64\n(1)Totalnumberofsharesincreases(2)Totalstockholders’equitydoesnotchange(3)Thecompositionofequitychanges(lessofretainedearnings;moreofstock)(4)StockdividendsrequirejournalentriesStockSplits:(1)Parvalueofasharedecreases(2)Totalnumberofsharesincreases(3)Totalstockholders’equitydoesnotchange(4)Thecompositionofequitydoesnotchange(sameamountsofstockandRE)(5)Stocksplitsdonotrequirejournalentries26.Describethereasonsthatacompanymayretireshares.简述企业取得库藏股的原因。★考核知识点:库藏股P307参见P307附4.26参考课件第8章TreasuryStock:Afirmmayalsobuyitsownsharesandholdthemforeventualresale.SuchsharesmaynotvoteatshareholdermeetingsorreceivedividendsWhyDoesACorporationReacquireItsOwnStock?(1)Reissuesharestoofficersandemployeesunderbonusandstockcompensationplans.因奖金和股票期权计划,再发行股票给高管喝雇员(2)Increasetradingofcompany'sstockinsecuritiesmarketinhopesofenhancingmarketvalue.增加本公司股票在证券市场的交易量,以希望提高市场价值(3)Haveadditionalsharesavailableforuseinacquisitionofothercompanies.为取得其他公司准备股票(4)Reducenumberofsharesoutstanding,therebyincreasingearningspershare.减少发行在外股数,以提高每股收益(5)Preventahostiletakeover.防止恶意并购27.Describethecharacteristicsofincomeandexpenses.简述收益和费用的特征。★考核知识点:收入与费用附4.27参考课件第9章28.Describethematchingmethodsbetweentheexpensesandrevenue.费用与收入配比的三种方法。64\n参考答案:Thematchingprincipleisbrokendownintothreepervasivemeasurementprinciples:费用的确认方法(即与收入配比的方法)(1)associatingcauseandeffect(因果关系):costsarerelativelyeasytoidentifywiththerelatedrevenues,suchasmaterialsanddirectlaborconsumedinthemanufacturingprocess(2)systematicandrationalallocation(系统合理的分配):costsaremorecloselyassociatedwithspecificaccountingperiods,suchascostsofbuildingsandequipment(3)immediaterecognition(立即确认):Allothercostsaregenerallyexpensedintheperiodinwhichtheyareincurred,suchasofficesalaries,utilities,advertisingexpenses,etc.★考核知识点:收入与费用配比P71-72参见P71-P72附4.28参考课件第9章29.Describethepurposesoffinancialstatementanalysis.简述财务报表分析的目的。参考答案:Financialstatementanalysishastwopurposes:(1)tousethepastperformanceofanentitytopredictitsfutureprofitabilityandcashflows.(2)toevaluatetheperformanceofanentitywithaneyetowardidentifyingproblemareas.★考核知识点:报表分析P437参见P437附4.29参考课件第10章30.Whatisthepurposeofastatementofcashflows?Howdoesitdifferfromabalancesheetandanincomestatement?说明现金流量表的作用,这与收益表和资产负债表的作用有何不同?参考答案:UsefulnessoftheIncomeStatement:(1)Evaluatepastperformance.评价过去业绩(2)Predictingfutureperformance.预测未来业绩(3)Helpassesstheriskoruncertaintyofachievingfuturecashflows.有助于评价达到未来现金流量的风险与不确定性Usefulnessofthebalancesheet:(1)Evaluatingthecapitalstructure.(2)Assessriskandfuturecashflows.(3)Analyzethecompany’s:Liquidity,solvency,andsinancialflexibility.PurposeoftheStatementofCashFlows:Toproviderelevantinformationaboutthecashreceiptsandcashpaymentsof64\nanenterpriseduringaperiod.Thestatementprovidesanswerstothefollowingquestions:Wheredidthecashcomefrom?Whatwasthecashusedfor?Whatwasthechangeinthecashbalance?Importanceofthestatementofcashflow:(1)Itisusefultomanagersinevaluatingpastoperationsandinplanningfutureinvestingandfinancingactivities.(2)Itisusefultoinvestors,creditors,andothersinassessingafirm’sprofitpotential.(3)Itisabasisforassessingthefirm’sabilitytopayitsmaturingdebt.★考核知识点:现金流量表P405参见P405附4.30参考课件第10章PurposeoftheStatementofCashFlows:Toproviderelevantinformationaboutthecashreceiptsandcashpaymentsofanenterpriseduringaperiod.Thestatementprovidesanswerstothefollowingquestions:Wheredidthecashcomefrom?Whatwasthecashusedfor?Whatwasthechangeinthecashbalance?Importanceofthestatementofcashflow:(1)Itisusefultomanagersinevaluatingpastoperationsandinplanningfutureinvestingandfinancingactivities.(2)Itisusefultoinvestors,creditors,andothersinassessingafirm’sprofitpotential.(3)Itisabasisforassessingthefirm’sabilitytopayitsmaturingdebt.Thestatementofcashflowsreportscashflowsbythreetypesofactivities:(1)Cashflowsfromoperatingactivities–transactionsthataffectnetincome.(2)Cashflowsfrominvestingactivities–transactionsthataffectnoncurrentassets.(3)Cashflowsfromfinancingactivities–transactionsthataffectequityanddebtoftheentity.31.Whatarethehorizontalanalysis,verticalAnalysisandratioanalysis?什么是横向分析、纵向分析、比率分析?★考核知识点:报表分析P436-451参见P436-P451附4.31参考课件第10章(1)Horizontalanalysis(ortrendanalysis):Usesdatafromprioryearsasayardstick.Theoldestyearisusedasabase,linebyline,andsubsequentyearsareexpressedasapercentageofthebase.Twosteps:64\n–selectabaseyearandassigneachitemonthebaseyearstatementaweightof100%;–expresseachitemfromthestatementsfortheotheryearsasapercentageofitsbaseyearamount(2)VerticalAnalysis:Apercentageanalysiscanbeusedtoshowtherelationshipofeachcomponenttoatotalwithinasinglestatement.Thetotal,or100%item,onthebalancesheetis“totalassets.”Netsalesis100.0%ontheincomestatement.Verticalanalysiswithbothdollarandpercentageamountsisalsousefulincomparingonecompanywithanotherorwithindustryaverages.Suchcomparisonsareeasiertomakewiththeuseofcommon-sizestatementsinwhichallitemsareexpressedinpercentages.(3)Ratioanalysis:Amathematicalrelationshipbetweentwoamountsfromthefinancialstatements.Theamountsmightconsistofasingleaccountoranumberofdifferentaccounts,fromanyofthefinancialstatements—thebalancesheet,theincomestatement,orthestatementofcashflow.§Solvencyistheabilityofabusinesstomeetitsfinancialobligations(debts)astheyaredue.Solvencyanalysisfocusesontheabilityofabusinesstopayorotherwisesatisfyitscurrentandnoncurrentliabilities.Thisabilityisnormallyassessedbyexaminingbalancesheetrelationships.§Profitabilityistheabilityofanentitytoearnprofits.Thisabilitytoearnprofitsdependsontheeffectivenessandefficiencyofoperationsaswellasresourcesavailable.Profitabilityanalysisfocusesprimarilyontherelationshipbetweenoperatingresultsreportedintheincomestatementandresourcesreportedinthebalancesheet.五、业务题1.RecordthefollowingselectedtransactionsforMarchinatwo-columnjournal,identifyingeachentrybyletter:(a)Received$10,000fromShirleyKnowles,owner.(b)Purchasedequipmentfor$35,000,paying$10,000incashandgivinganotepayablefortheremainder.(c)Paid$1,000forrentforMarch.(d)Purchased$8,500ofsuppliesonaccount.(e)Recorded$2,500offeesearnedonaccount.(f)Received$11,000incashforfeesearned.(g)Paid$200tocreditorsonaccount.64\n(h)Paidwagesof$1,250.(i)Received$1,150fromcustomersonaccount.(j)Recordedowner'swithdrawalof$1,850.ANS:(a)Cash10,000ShirleyKnowles,Capital10,000(b)Equipment35,000Cash10,000NotesPayable25,000(c)RentExpense1,000Cash1,000(d)Supplies8,500AccountsPayable8,500(e)AccountsReceivable2,500FeesEarned2,500(f)Cash11,000FeesEarned11,000(g)AccountsPayable200Cash200(h)WagesExpense1,250Cash1,250(i)Cash1,150AccountsReceivable1,150(j)ShirleyKnowles,Drawing1,850Cash1,850★考核知识点:借贷复式记账P38参见P38附5.1参考课件第4章Thedouble-entrysystem:lAsystemofrecordingtransactionsinawaythatmaintainstheequalityoftheaccountingequation.lThefundamentalruleofdouble-entrybookkeepingisthatdebitsmust64\nequalcredits.lForeverytransaction,theremustbeatleastonedebitandonecredit.lDebitsmustalwaysequalcreditsforeachtransaction.lDebitsarealwaysenteredontheleftsideofanaccountandcreditsarealwaysenteredontherightside.2.JournalizethesixentriesthatadjusttheaccountsatDecember31.Oneoftheaccountswasaffectedbytwodifferentadjustingentries.UnadjustedTrialBalanceAdjustedTrialBalanceCash3,0003,000AccountsReceivable30,00030,500Supplies1,700100PrepaidInsurance2,000400Equipment9,0009,000AccumulatedDepreciation1,500WagesPayable4,000UnearnedFees6,0001,500AnnCole,Capital20,00020,000FeesEarned62,00067,000WagesExpense42,30046,300SuppliesExpense1,600InsuranceExpense1,600DepreciationExpense1,500Total88,00088,00094,00094,000========================ANS:AccountsReceivable500FeesEarned500SuppliesExpense1,600Supplies1,600InsuranceExpense1,600PrepaidInsurance1,600DepreciationExpense1,500AccumulatedDepreciation1,500UnearnedFees4,50064\nFeesEarned4,500WagesExpense4,000WagesPayable4,000★考核知识点:调整分录P72-81参见P72-P81附5.2参考课件第4章3.Foreachofthefollowing,journalizethenecessaryadjustingentry:(a)Abusinesspaysweeklysalariesof$15,000onFridayforafive-dayweekendingonthatday.Journalizethenecessaryadjustingentryattheendofthefiscalperiod,assumingthatthefiscalperiodends(1)onWednesday,(2)onThursday.(b)Thebalanceintheprepaidinsuranceaccountbeforeadjustmentattheendoftheyearis$14,000.Journalizetheadjustingentryrequiredundereachofthefollowingalternatives:(1)theamountofinsuranceexpiredduringtheyearis$4,500,(2)theamountofunexpiredinsuranceapplicabletoafutureperiodis$1,500.(c)OnJuly1ofthecurrentyear,abusinesspays$36,000tothecityforlicensetaxesforthecomingfiscalyear.Thesamebusinessisalsorequiredtopayanannualpropertytaxattheendoftheyear.Theestimatedamountofthecurrentyear'spropertytaxallocabletoJulyis64\n$3,200.(1)JournalizethetwoadjustingentriesrequiredtobringtheaccountsaffectedbythetaxesuptodateasofJuly31.(2)WhatistheamountoftaxexpenseforJuly?(d)Theestimateddepreciationonequipmentfortheyearis$24,000.ANS:(a)(1)SalaryExpense9,000SalariesPayable9,000(2)SalaryExpense12,000SalariesPayable12,000(b)(1)InsuranceExpense4,500PrepaidInsurance4,500(2)InsuranceExpense12,500PrepaidInsurance12,500(c)(1)TaxesExpense3,000PrepaidLicenseTaxes3,000TaxesExpense3,200PropertyTaxesPayable3,200(2)$6,200($3,000+$3,200)(d)DepreciationExpense24,000AccumulatedDepreciation-Equipment24,000★考核知识点:调整分录P72-81参见P72-P81附5.3参考课件第4章(同上)4.OnthebasisofthefollowingdatatakenfromtheAdjustedTrialBalancecolumnsoftheworksheetfortheyearendedOctober31forShoreCo.,journalizethefourclosingentries.Cash$21,500AccountsReceivable45,200Supplies5,000Equipment169,900AccumulatedDepreciation$69,000AccountsPayable42,500StanShore,Capital152,600StanShore,Drawing30,00064\nFeesEarned404,500SalaryExpense300,500RentExpense60,000DepreciationExpense25,000SuppliesExpense9,500MiscellaneousExpense2,000$668,600$668,600================ANS:Oct.31FeesEarned404,500IncomeSummary404,50031IncomeSummary397,000SalaryExpense300,500RentExpense60,000DepreciationExpense25,000SuppliesExpense9,500MiscellaneousExpense2,00031IncomeSummary7,500StanShore,Capital7,50031StanShore,Capital30,000StanShore,Drawing30,000★考核知识点:结账分录P102参见P102附5.4参考课件第4章TheClosingProcess:(1)Debiteachrevenueaccountfortheamountofitsbalance,andcreditIncomeSummaryforthetotalrevenue.(2)DebitIncomeSummaryforthetotalexpensesandcrediteachexpenseaccountforitsbalance.(3)DebitIncomeSummaryfortheamountofitsbalance(inthiscase,thenetincome)andcreditthecapitalaccount.(4)Debitthecapitalaccountforthebalanceofthedrawingaccount,andcreditdrawingforthesameamount.Aftertheclosingentriesareposted,allofthetemporaryaccountshavezerobalances.64\n5.ThebankstatementforAllenCo.indicatesabalanceof$8,000.00onJune 30,2005.AfterthejournalsforJunehadbeenposted,thecashaccounthadabalanceof$3,675.00.Prepareabankreconciliationonthebasisofthefollowingreconcilingitems:(a)Cashsalesof$342hadbeenerroneouslyrecordedinthecashreceiptsjournalas$324.(b)Depositsintransitnotrecordedbybank,$500.00.(c)Bankdebitmemorandumforservicecharges,$25.00.(d)Bankcreditmemorandumfornotecollectedbybank,$2850,including$50interest.(e)Bankdebitmemorandumfor$218.00NSF(notsufficientfunds)checkfromAliceBell,acustomer.(f)Checksoutstanding,$2,200.00.ANS:AllenCo.BankReconciliationJune30,2005Cashbalanceaccordingtobankstatement$8,000.00Adddepositsintransitnotrecordedbybank500.00$8,500.00Deductoutstandingchecks2,200.00Adjustedbalance$6,300.00=========Cashbalanceaccordingtodepositor'srecords$3,675.00Add:Notecollectedbybank,including$50interest$2,850.00Errorinrecordingcashsalesof$342as$32418.002,868.00$6,543.00Deduct:NSFcheckfromAliceBell$218.00Bankservicecharges25.00243.00Adjustedbalance$6,300.00=========★考核知识点:银行调节表P200参见P200附5.5参考课件第5章64\nAbankreconciliationisalistingoftheitemsandamountsthatcausethecashbalancereportedinthebankstatementtodifferfromthebalanceofthecashaccountintheledger.Reasonsfordifferencesbetweendepositor’srecordsandthebankstatement:(1)Outstandingchecks.(2)Depositsintransit.(3)Servicecharges(4)Collections(5)Not-sufficient-funds(NSF)checks(6)Errors6.Usingthefollowinginformation,prepareabankreconciliationforColeCo.forMay31ofthecurrentyear:(a)Thebankstatementbalanceis$3,012.(b)Thecashaccountbalanceis$3,165.(c)Outstandingchecksamountedto$590.(d)Depositsintransitare$704.(e)Thebankservicechargeis$30.(f)Acheckfor$76forsupplieswasrecordedas$67intheledger.ANS:ColeCo.BankReconciliationMay31,2005Cashbalanceaccordingtobankstatement$3,012Adddepositsintransitnotrecordedbybank704$3,716Deductoutstandingchecks590Adjustedbalance$3,126======Cashbalanceaccordingtodepositor'srecords$3,165Deduct:Bankservicecharge$30Errorinrecording939Adjustedbalance$3,126======★考核知识点:银行调节表P200参见P200附5.6参考课件第5章(同上)64\n7.Forabusinessthatmakesadvanceprovisionforuncollectiblereceivables(a)Journalizetheentriestorecordthefollowing:(1)RecordtheadjustingentryatDecember31,theendofthefiscalyear,toprovidefordoubtfulaccounts.Theaccountsreceivableaccounthasabalanceof$800,000,andthecontraassetaccountbeforeadjustmenthasadebitbalanceof$600.Analysisofthereceivablesindicatesdoubtfulaccountsof$20,000.(2)InMarchofthefollowingfiscalyear,the$550owedbyFlakeCo.onaccountiswrittenoffasuncollectible.(3)Eightmonthslater,$200oftheFlakeCo.accountisreinstatedandpaymentofthatamountisreceived.(4)InOctober,$400isreceivedonthe$600owedbyDoeCo.andtheremainderiswrittenoffasuncollectible.(b)Basedonthedatain(a)(1)above,whatisthenetrealizablevalueof theaccountsreceivableasreportedonthebalancesheetasofDecember 31?(c)Assumingthatthebusinesshadbeenfollowingthedirectwrite-offprocedureinaccountingforuncollectiblereceivables,journalizetheentriestorecordthefollowing:(1)Recordedthewrite-offofaccountofFlakeCo.[(a)(2)above].(2)ReinstatedaccountofFlakeCo.for$200andrecordedpaymentofthatamountreceived[(a)(3)above].(3)Recordedthereceiptof$400fromDoeCo.in(a)(4)aboveandwroteofftheremainderowedasuncollectible.ANS:(a)(1)UncollectibleAccountsExpense20,600AllowanceforDoubtfulAccounts20,600(2)AllowanceforDoubtfulAccounts550AccountsReceivable-FlakeCo550(3)AccountsReceivable-FlakeCo200AllowanceforDoubtfulAccounts200Cash200AccountsReceivable-FlakeCo200(4)Cash40064\nAllowanceforDoubtfulAccounts200AccountsReceivable-DoeCo600(b)$780,000($800,000-$20,000)(c)(1)UncollectibleAccountsExpense550AccountsReceivable-FlakeCo550(2)AccountsReceivable-FlakeCo200UncollectibleAccountsExpense200Cash200AccountsReceivable-FlakeCo200(3)Cash400UncollectibleAccountsExpense200AccountsReceivable-DoeCo600★考核知识点:应收账款坏账处理P212-217参见P212-P217附5.7参考课件第5章MethodsofAccountingforUncollectibleAccounts:(1)TheAllowanceMethod:§Thismethodisconsistentwiththematchingprinciple.§Managementmakesanestimateeachyearoftheportionofaccountsreceivablethatmaynotbecollectible.§UncollectibleAccountsExpense(BadDebts)isdebitedandAllowanceforDoubtfulAccountsiscredited.§ActualaccountsthatprovetobeuncollectiblearedebitedtoAllowanceforDoubtfulAccountsandcreditedtoAccountsReceivable.(2)DirectWrite-OffMethod:Theoreticallyundesirable:nomatching;receivablenotstatedatnetrealizablevalue8.Thebeginninginventoryandpurchasesofanitemfortheperiodwereasfollows:Beginninginventory6unitsat$73eachFirstpurchase10unitsat$72eachSecondpurchase18unitsat$74eachThirdpurchase10unitsat$75each64\nThecompanyusestheperiodicsystem,andtherewere15unitsintheinventoryattheendoftheperiod.Determinethecostofthe15unitsintheinventorybyeachofthefollowingmethods,presentingdetailsofyourcomputations:(a)first-in,first-out;(b)last-in,first-out;(c)averagecost.ANS:(a)10units@$75$7505units@$74370Total$1,120======(b)6units@$73$4389units@$72648Total$1,086======(c)Averageunitcost=$73.64$3,240/4415units@$73.64=$1,104.60=========★考核知识点:存货计价P239-245参见P239-P245附5.8参考课件第5章Acompanyusingaperpetualsystemmaintainsacontinuousrecordofthephysicalquantitiesinitsinventory.OpeningInventory+Purchases-GoodsSold=ClosingInventoryAcompanyusingaperiodicsystemdoesnotmaintainsacontinuousrecordofthephysicalquantitiesonhand.OpeningInventory+Purchases-ClosingInventory=GoodsSold(1)First-in,First-out(FIFO)methodassumesthattheearliestgoodspurchasedarethefirsttobesold.Thus,costofgoodssoldisobtainedbytakingtheunitcostoftheoldestgoodspurchasedandworkingforwarduntilthecostofallunitssoldhavebeendetermined.Asaresult,endinginventoryisthemostrecentlypurchasedgoods.(2)Last-in,First-out(LIFO)methodassumesthatthelastgoodspurchasedarethefirsttobesold.Thus,costofgoodssoldisobtainedbytakingtheunitcostofthemostrecentlypurchasedgoodsandworkingbackwarduntilthecostofallunitssoldhavebeendetermined.Asaresult,endinginventoryistheoldestpurchasedgoods.64\n(3)Averagecostmethodassumesthatthegoodsavailableforsalearehomogeneousandallocatesthecostofgoodsavailableforsaleonthebasisoftheweightedaverageunitcostincurred.Theweightedaverageunitcostisthenappliedtotheunitssoldtodeterminethecostofgoodssold.Inaddition,itisappliedtotheunitsinendinginventorytodeterminethevalueofendinginventory.9.Thefollowingdataregardingpurchasesandsalesofacommodityweretakenfromtherelatedperpetualinventoryaccount:May1Balance25unitsat$406Sale20units8Purchase20unitsat$4116Sale10units20Purchase20unitsat$4223Sale25units30Purchase15unitsat$43(a)DeterminethecostoftheinventorybalanceatMay31,using(1)thefirst-in,first-outmethodand(2)thelast-in,first-outmethod.Identifythequantity,unitprice,andtotalcostofeachlotintheinventory.(b)Presentthejournalentrytorecordashortage(shrinkage)of$53discoveredbythephysicalcountonMay31.ANS:(a)(1)May2010unitsat$42$4203015unitsat$43645Total$1,065======(2)May15unitsat$40$20085unitsat$412053015unitsat$43645Total$1,050======(b)InventoryShrinkage(orCostofMerchandiseSold)53MerchandiseInventory5364\n★考核知识点:存货计价P239-245参见P239-P245附5.9参考课件第5章(同上)10.PresententriestorecordthefollowingselectedtransactionsofBeltonCo.(a)Purchased500sharesofthe100,000sharesoutstanding$10parcommonsharesofDenverCorporationfor$5,100,asinvestmentinavailable-for-salesecurities.(b)Purchased2,000sharesofthe10,000sharesnoparcommonsharesofReillyCo.for$45,600.Theinvestmentwasaccountedforbytheequitymethod.(c)Receivedacashdividendof$1pershareontheDenverCorporationstockacquiredin(a).(d)Receivedacashdividendof$2pershareontheReillyCo.stockacquiredin(b).(e)Sold100sharesoftheDenverCorporationsharesacquiredin(a)for$2,100.(f)RecordedtheappropriateshareofReilly'sCo.netincomeof$50,000.Thestockwasacquiredin(b).ANS:(a)Available-for-salesecurities5,100Cash5,100(b)InvestmentinReillyCo.Stock45,600Cash45,600(c)Cash500DividendRevenue500(d)Cash4,000InvestmentinReillyCo.Stock4,000(e)Cash2,100Available-for-salesecurities1,020GainonSaleofAvailable-for-salesecurities1,080(f)64\nInvestmentinReillyCo.Stock10,000IncomeofReillyCo.10,000★考核知识点:股票投资P361-365参见P361-P365附5.10参考课件第6章GAAPtreatmentof“available-for-sale”securitiesismoreinvolved.Ittreatsholdinggainsandlossesasequity(i.e.,balancesheet)adjustments,NOTincomestatementadjustments.Increasesinbookvaluearerecordedonthebalancesheetasunrealizedholdinggainsonmarketablesecurities–available-for-sale.Decreasesinbookvaluearerecordedonthebalancesheetasunrealizedholdinglossesonmarketablesecurities–available-for-sale.Significantinfluenceisnormallyassumedtoexistiftheinvestorholds20%ormoreofthevotingequityoftheinvestee.Undertheequitymethodofaccounting,theinvestmentisinitiallyrecordedatthepurchasepriceinaninvestmentsaccount.Subsequenttoacquisition,theinvestmentaccountisincreasedordecreasedbytheinvestor’sshareoftheprofitorlossesoftheinvesteeandreducedbytheinvestor’sshareofdividendsfromtheinvestee.11.PreparethejournalentriesforthefollowingtransactionsforMillerCo.(a)MillerCo.purchased25,000sharesofthetotalof100,000sharesofBudCorp.stockfor$10pershareplusa$400commission.(b)BudCorp.'stotalearningsfortheperiodare$80,000.(c)BudCorp.paidatotalof$45,000incashdividends.ANS:(a)InvestmentinBudCorp.Stock250,400Cash250,400(b)InvestmentinBudCorp.Stock20,000IncomeofBudCorp.20,000(c)Cash11,250InvestmentinBudCorp.Stock11,250★考核知识点:股票投资---权益法P363参见P363附5.11参考课件第6章64\nSignificantinfluenceisnormallyassumedtoexistiftheinvestorholds20%ormoreofthevotingequityoftheinvestee.However,ifitcanbedemonstratedthataholdingof20%ormoreofthevotingequitydoesnotgivesignificantinfluence,theinvestmentwouldnotbeconsideredaninvestmentinanassociate.Similarly,ifitcanbedemonstratedthataholdingoflessthan20%ofthevotingequityoftheinvesteedoesleadtosignificantinfluence,theinvestmentwouldbeconsideredaninvestmentinanassociate.Wherethereisnoparent-subsidiaryrelationshipbuttheinvestorisabletoexercisesignificantinfluenceovertheoperating,investing,andfinancingdecisionsoftheinvestee,thestrategicinvestmentshouldbeaccountedforusingtheequitymethod.Undertheequitymethodofaccounting,theinvestmentisinitiallyrecordedatthepurchasepriceinaninvestmentsaccount.Subsequenttoacquisition,theinvestmentaccountisincreasedordecreasedbytheinvestor’sshareoftheprofitorlossesoftheinvesteeandreducedbytheinvestor’sshareofdividendsfromtheinvestee.Anydifferencebetweenthepurchasepriceandtheunderlyingequityinnetassetsoftheacquiredcompanyisamortizedbasedonanallocationofthepurchasepricetospecificassets.Anydifferencethatcannotberelatedtospecificassetsisclassifiedasgoodwill,whichistestedforimpairmentoveritsusefullife.12.AceCompanypurchasedasalong-terminvestment$500,000ofBlueCorporation10-year,9%bonds.Presententriestorecordthefollowingselectedtransactions:(a)Purchasedbondsfor$475,000.(b)Amortized$1,800ofdiscountonbondsfortheyear.(c)Soldbondsat98plusaccruedinterestof$8,000.Thebrokerdeducted$400forbrokeragefeesandtaxes,remittingthebalance.Thebondswerecarriedat$489,000atthetimeofthesale.ANS:(a)InvestmentinBlueCorporationBonds475,000Cash475,000(b)InvestmentinBlueCorporationBonds1,800InterestRevenue1,800(c)Cash497,60064\nInterestRevenue8,000InvestmentinBlueCorp.Bonds489,000GainonSaleofInvestments600★考核知识点:长期债券投资P388-390参见P388-P390附5.12参考课件第6章Investmentsindebtsecuritiesareinitiallyrecordedatthepricepaidfortheobligation,whichmayormaynotbethefacevalue.Atsubsequentfinancialreportingdates,theinvestmentisremeasuredtoitsfairvalueatthefinancialreportingdate.Classifyadebtsecurityasheld-to-maturityonlyifithasboth:thepositiveintentandtheabilitytoholdsecuritiestomaturity.Thesupportingrationaleliesinthefactthattheentitywillholdtheassetuntilitsfinalmaturity.Asaresult,temporaryfluctuationsinmarketvaluearenotanissue.Accountedforatamortizedcost,notfairvalue.Amortizepremiumordiscountusingtheeffective-interestmethodunlessthestraight-linemethod—yieldsasimilarresult.13.JournalizetheentriestorecordthefollowingselectedtransactionsofOwensCo.:(a)Purchased$100,000ofKellyCo.8%bondsat102plusaccruedinterestof$2,000.(b)Receivedfirstsemiannualinterestpayment.(c)Amortized$40onthebondinvestmentattheendofthefirstyear.(d)Soldthebondsat97plusaccruedinterestof$1,500.Thebondswerecarriedat$101,500atthetimeofthesale.ANS:(a)InvestmentinKellyCo.Bonds102,000InterestRevenue2,000Cash104,000(b)Cash4,000InterestRevenue4,000(c)InterestRevenue40InvestmentinKellyCo.Bonds40(d)64\nCash98,500LossonSaleofInvestments4,500InvestmentinKellyCo.Bonds101,500InterestRevenue1,500★考核知识点:长期债券投资P388-390参见P388-P390附5.13参考课件第6章(同上)14.Equipmentpurchasedatthebeginningofthefiscalyearfor$150,000isexpectedtohaveausefullifeof5years,or15,000operatinghours,andaresidualvalueof$30,000.Computethedepreciationforthefirstandsecondyearsofusebyeachofthefollowingmethods:(a)straight-line(b)units-of-production(2,500hoursfirstyear;3,250hourssecondyear)(c)declining-balanceattwicethestraight-linerate(Roundtheanswertothenearestdollar.)ANS:1stYear(a)$24,000($150,000-30,000)=120,000÷5(b)$20,000($150,000-30,000)=($120,000÷15,000hours)=$8/hrx2,500(c)$60,000($150,000x.40)2ndYear(a)$24,000($150,000-30,000)=120,000÷5(b)$26,000($150,000-30,000)=($120,000÷15,000hours)=$8/hrx3,250(c)$36,000($150,000-60,000)=90,000x.40★考核知识点:折旧方法P261-264参见P261-P264附5.14参考课件第6章(1)Straight-linedepreciationisthemostwidelyusedmethodofdepreciation.Underthestraight-linemethod,depreciationisthesameforeachyearoftheasset'susefullife.Annualdepreciation=(Cost–estimatedresidualvalue)/Estimatedlife(2)Undertheunits-of-Productionmethod,thelifeofanassetisexpressedintermsofthetotalunitsofproductionortheuseexpectedfromtheasset.Depreciationperunit,hour,etc.=(Cost–estimatedresidualvalue)/Estimatedlifeinunits,hours,etc.(3)Thedeclining-balancemethodisanacceleratedmethod.Acceleratedmethodsofdepreciationresultinmoredepreciationintheearlyyearsofanasset'slifeandlessdepreciationinthelateryearsofanasset'slifethandoesthestraight-lineapproach.64\nDeclining-BalanceMethod:Utilizesadepreciationrate(%)thatissomemultipleofthestraight-linemethod.Doesnotdeducttheresidualvalueincomputingthedepreciationbase.15.MachineryispurchasedonJuly1ofthecurrentfiscalyearfor$180,000.Itisexpectedtohaveausefullifeof4years,or20,000operatinghours,andaresidualvalueof$15,000.ComputethedepreciationforthelastsixmonthsofthecurrentfiscalyearendingDecember31byeachofthefollowingmethods:(a)straight-line(b)declining-balanceattwicethestraight-linerate(c)units-of-production(usedfor1,500hoursduringthecurrentyear)(Roundtheanswertothenearestdollar.)ANS:(a)$20,625=($180,000-15,000)=165,000÷4=41,250´6/12(b)$45,000=($180,000´.50)=$90,000´6/12(c)$12,375=($180,000-15,000)=($165,000÷20,000hours)=$8.25´1,500hours★考核知识点:折旧方法P261-264参见P261-P264附5.15参考课件第6章(同上)16.Computerequipment(officeequipment)purchased61/2yearsagofor$170,000,withanestimatedlifeof8yearsandaresidualvalueof$10,000,isnowsoldfor$60,000cash.(Appropriateentriesfordepreciationhadbeenmadeforthefirstsixyearsofuse.)Journalizethefollowingentries:(a)Recordthedepreciationfortheone-halfyearpriortothesale,usingthestraight-linemethod.(b)Recordthesaleoftheequipment.(c)Assumingthattheequipmenthadbeensoldfor$30,000cash,preparetheentryfor(b)abovetorecordthesale.ANS:(a)DepreciationExpense-OfficeEquipment10,000AccumulatedDepreciation-OfficeEquipment10,000(b)Cash60,000AccumulatedDepreciation-OfficeEquipment130,000OfficeEquipment170,000GainonSaleofFixedAssets20,000(c)Cash30,00064\nAccumulatedDepreciation-OfficeEquipment130,000LossonDisposalofFixedAssets10,000OfficeEquipment170,000★考核知识点:固定资产处置P268-269参见P268-P269附5.16参考课件第6章Whenfixedassetslosetheirusefulnesstheymaybedisposedofinoneofthefollowingways:discarded,sold,or.traded(exchanged)forsimilarassets.Requiredentrieswillvarywithtypeofdispositionandcircumstances,butthefollowingentrieswillalwaysbenecessary:Anassetaccountmustbecreditedtoremovetheassetfromtheledger,andtherelatedAccumulatedDepreciationaccountmustbedebitedtoremoveit’sbalancefromtheledger.Whenfixedassetsaresold,theownermaybreakeven,sustainaloss,orrealizeagain.1.Ifthesalepriceisequaltobookvalue,therewillbenogainorloss.2.Ifthesalepriceislessthanbookvalue,therewillbealossequaltothedifference.3.Ifthesalepriceismorethanbookvalue,therewillbeagainequaltothedifference17.Journalizethefollowingentriesonthebooksoftheborrowerandcreditor.Labelaccordingly.Jun.1RobertsCo.purchasedmerchandiseonaccountfromWrightCo.,$60,000,termsn/30.Jun.30RobertsCo.issueda60-day,5%notefor$60,000onaccount.Aug.29RobertsCo.paidtheamountdue.ANS:RobertsCo.(Borrower)June1MerchandiseInventory60,000AccountsPayable60,00030AccountsPayable60,000NotesPayable60,000Aug.29NotesPayable60,000InterestExpense500Cash60,500WrightCo.(Creditor)64\nJune1AccountsReceivable60,000Sales60,00030NotesReceivable60,000AccountsReceivable60,000Aug.29Cash60,500NotesReceivable60,000InterestRevenue500★考核知识点:商品购销—应收账款、应收票据P219-221;应付账款、应付票据P286-287参见P286-P287附5.17参考课件第6章、第7章Tradeaccountspayablearisefromthepurchaseofinventory,supplies,orservicesoncredit.Anotepayableisanunconditionalwrittenagreementtopayasumofmoneytothebeareronaspecificdate.Notesmaybeissuedwhenmerchandiseandotherassetsarepurchased.Theymayalsobeissuedtocreditor'stotemporarilysatisfyanaccountpayablecreatedearlierandmaybeissuedwhenmoneyisborrowedfrombanks.18.ArthurCorp.issued$2,500,000of20-year,9%callablebondsonJuly1,2005,withinterestpayableonJune30andDecember31.Thefiscalyearofthecompanyisthecalendaryear.Journalizetheentriestorecordthefollowingselectedtransactions:2005July1Issuedthebondsforcashattheirfaceamount.Dec.31Paidtheinterestonthebonds.2011Dec.31Calledthebondissueat97,therateprovidedinthebondindenture.(Omitentryforpaymentofinterest.)ANS:2005July1Cash2,500,000BondsPayable2,500,000Dec.31InterestExpense112,50064\nCash112,5002011Dec.31BondsPayable2,500,000GainonRedemptionofBonds75,000Cash2,425,000★考核知识点:债券发行P383-388参见P383-P388附5.18参考课件第7章IfNominalrate=effectiverate,PVofthefuturecashflows,discountedattheeffectiveinterestrate,willequalthefacevalueofthedebtIfNominalrate>effectiverate,PVofthefuturecashflowswillhigherthanthefacevalueofthedebt,thebondwillsellforapremium.IfNominalrate

-

关注微信公众号售出明细实时看

关注微信公众号售出明细实时看